Data from UK consultancy Cornwall Insight shows that profits for battery storage units will rebound by 2026 after “an extended period of underperformance”.

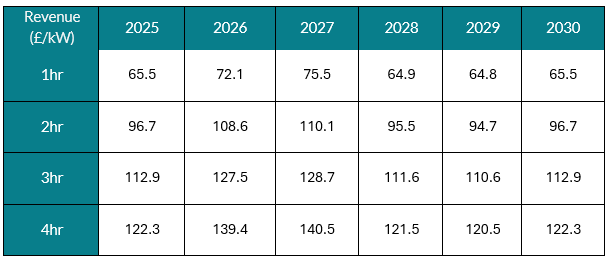

The firm’s GB Battery Revenue Forecast shows that annual revenues for 2-hour assets are set to increase from around £96/kW in 2025 to £108/kW by 2026, with other durations observing similar growth, Cornwall Insight said. This is attributed to rising wholesale prices, added price volatility and renewables build out over the coming years.

A small slowdown in yearly revenues is forecast towards the end of the decade in line with Cornwall Insight’s wholesale power price projections alongside greater battery storage market saturation. Those levels will sit above where they currently are, however.

Lead analyst at Cornwall Insight Joe Camish said: “After a challenging period for battery asset owners in GB, we are forecasting a recovery in battery storage revenues over the next two years. This will be encouraging news for investors and asset owners, signalling a more robust and sustainable future for battery storage investments for the remainder of the decade.

“This has been underscored by our recent modelling in which revenue levels are projected to remain above current levels, supported by greater wholesale price volatility in the late 2020s.”

Investment in the battery storage sector will be critical, particularly following the newly-established National Energy System Operator’s (NESO) suggestion that storage capacity in the UK will have to increase fivefold in order to achieve government-set clean power targets.

UK battery revenues hit a peak in August, according to analysis by Modo Energy, which reported that battery energy storage systems (BESS) earned the second highest daily total revenue in 2024 so far, reaching a high of £250/MW, on 21 August.

So far in 2024, Britain has seen prices fall below zero for a total of 147 hours – 44 more than the entire of 2023. Modo Energy forecasts that negative-priced hours will total 188 hours by the end of the year. This rise in negative-priced periods contributed to a rise in BESS revenues for late August.

Further, Modo reported that on 21 August, UK BESS systems provided over 600MW of power to the grid through the Balancing Mechanism (BM), boosting the sale price to £47/MW in addition to their wholesale and frequency response revenues.

Battery developers recently criticised BESS’ (lack of) involvement in the BM and called on NESO to improve battery skip rates—the frequency with which the system operator skips over batteries to use more expensive methods. By the middle of November, NESO will publish an LCP Delta definition, methodology, and full report on skip rates, and by the end of November, it will deploy new transparency tools.